In a key ruling in favour of thousands of Polish borrowers who took out billions in foreign-currency mortgages, the European Court of Justice (ECJ) has found that banks cannot demand extra fees for loan contracts that have been invalidated due to unlawful clauses.

The decision has been welcomed by borrowers, who regard the practice of banks demanding additional payment for what they call “non-contractual use of capital” during the course of an invalidated loan as a way to discourage them from pursuing claims.

However, the ruling – which analysts believe could cost the banking sector as much as 100 billion zloty (€22.44 billion) – has been criticised by Poland’s financial authority.

#ECJ: Annulment of a mortgage #loan agreement containing #unfairterms: #EU law doesn’t preclude #consumers from seeking compensation from the bank going beyond reimbursement of the monthly instalments paid 👉https://t.co/ATb3CgbPxg

— EU Court of Justice (@EUCourtPress) June 15, 2023

“EU law does not preclude, in the event of the annulment of a mortgage loan agreement vitiated by unfair terms, the consumers from seeking compensation from the bank going beyond reimbursement of the monthly instalments paid,” the court ruled.

“By contrast, it [the law] precludes the bank from relying on similar claims against consumers,” added the ECJ in its announcement of the ruling this morning.

The ruling, which confirmed an earlier opinion issued by the ECJ’s advocate general, will affect an estimated 130,000 cases pending before Polish courts in a longstanding dispute between banks and borrowers of mortgages in foreign currencies, mainly Swiss francs.

Those borrowers saw their repayments skyrocket following the zloty’s weakening against the franc and who found out that their contracts contained clauses not permitted under the law.

Polish banks' shares fell after the EU court's advocate general issued an opinion on a case relating to foreign-currency mortgages that have been invalidated in Poland.

He found that banks may not pursue claims for the use of capital from such loans https://t.co/hMTRoFZYI4

— Notes from Poland 🇵🇱 (@notesfrompoland) February 16, 2023

In many cases, courts ruled to invalidate contracts containing such clauses. After the annulment of the faulty contract, the customer had to return to the bank the capital they had received, and the bank would return all instalments and fees charged to the customer, plus interest.

Some banks, however, began to demand payment for the non-contractual use of the capital during the period of the invalidated contract, arguing that their customers had made a profit through, for example, appreciation of the value of a property. Faced with these arguments, Warsaw’s district court asked the ECJ to clarify its case law.

“Any annulment of the mortgage loan agreement is a consequence of [the] bank[s] use of unfair terms,” found the ECJ. “Therefore, it can neither be accepted that the bank derive economic advantages from its unlawful conduct, nor that it be compensated for the disadvantages caused by such conduct.”

In addition, the court found that the banking sector’s argument about the need to ensure the stability of the financial markets was not relevant when interpreting EU regulations aimed at protecting consumers.

The ECJ has said that Polish judges must decide how to deal with cases concerning almost €26 billion in foreign-currency mortgages.

Poland's Supreme Court is expected to soon issue a landmark ruling that could have major financial consequences for banks https://t.co/91Lq6uHGyi

— Notes from Poland 🇵🇱 (@notesfrompoland) April 30, 2021

The ECJ also ruled in a parallel case that a borrower cannot be denied the suspension of loan repayments after filing a lawsuit against the bank, even if they have not yet paid down the entire principal.

Although in many cases consumers were allowed to stop repayments during the ongoing case if there was a suspicion their contract might contain faulty clauses, some courts refused to withhold repayments, arguing that the bank was in a bad position.

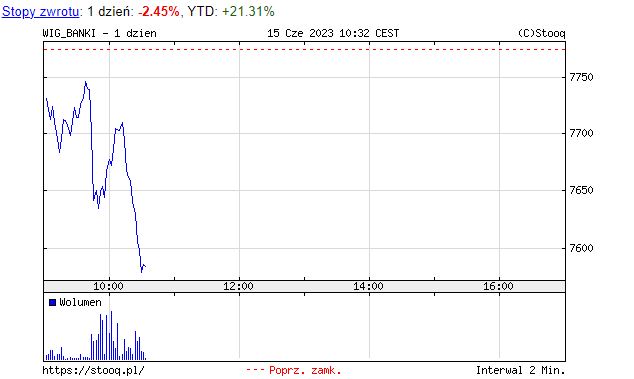

Both cases are seen as key for Poland’s banking sector. After the ruling was announced, the banking sub-index of the Warsaw Stock Exchange lost 2.45% on the day an hour after the ruling.

Source: stooq.pl

“This [ruling] may result in a new wave of lawsuits, as so far some consumers may have feared claims by financial institutions after the cancellation of a credit agreement,” said Bartosz Sawicki, an analyst with currency exchange website Cinkciarz.pl.

He noted that, according to the Polish Financial Supervision Authority (KNF), the total costs for financial institutions could be as high as 100 billion zloty.

“At the same time, today’s ruling should increase the willingness of banks to reach settlements, the number of which has exceeded 40,000 in the last two years,” added Sawicki.

The ruling was criticised by the KNF, which wrote that it had “a negative dimension from the point of view of the Polish banking sector and the Polish economy as a whole, but also from the point of view of legal certainty, public interest and elementary principles of social justice, granting preferential treatment to a narrow group of borrowers in the form of ‘free credit’.”

KNF krytycznie i ostro o wyroku TSUE: ma negatywny wymiar z punktu widzenia PL sektora bankowego oraz całej PL gospodarki, ale także z punktu widzenia pewności prawa, interesu publicznego oraz elementarnych zasad sprawiedliwości społecznej https://t.co/HLNzlqZ31m

— Bartek Godusławski (@BGoduslawski) June 15, 2023

The problem of foreign-currency mortgages has animated debate in Poland for more than a decade. Hundreds of thousands of Poles took out such loans to take advantage of low-interest rates on the Swiss franc.

Later, however, many struggled to pay back instalments when the Swiss currency sharply appreciated against the Polish zloty after the 2008 financial crisis and when it was unpegged from the euro in 2015.

Currently, borrowers also have to cope with rising interest rates in Switzerland, which, although still well below the 6.75% level maintained by the Polish central bank, reached 1.5% in March, the highest since October 2008.

As of April, active foreign currency mortgages in Poland were still worth 69.5 billion zloty (€15.60 billion), with Swiss franc mortgages amounting to 44.5 billion złoty (€9.98 billion), according to the Polish Financial Supervision Authority (KNF).

The Supreme Court has again delayed a key ruling concerning billions of euros of foreign-currency loans

The latest postponement related to doubts over whether, because of the government’s contested judicial reforms, some judges were legitimately appointed https://t.co/fzpXSl0vzW

— Notes from Poland 🇵🇱 (@notesfrompoland) September 3, 2021

Main image credit: Swiss National Bank

Alicja Ptak is deputy editor-in-chief of Notes from Poland and a multimedia journalist. She has written for Clean Energy Wire and The Times, and she hosts her own podcast, The Warsaw Wire, on Poland’s economy and energy sector. She previously worked for Reuters.